FAM-L Exam Solutions and Hints#

actuarialmath – Solving Life Contingent Risks with Python

This package implements fundamental methods for modeling life contingent risks, and closely follows traditional topics covered in actuarial exams and standard texts such as the “Fundamentals of Actuarial Math - Long-term” exam syllabus by the Society of Actuaries, and “Actuarial Mathematics for Life Contingent Risks” by Dickson, Hardy and Waters. These code chunks demonstrate how to solve each of the sample FAM-L exam questions released by the SOA.

Sources:

SOA FAM-L Exam Questions: copy retrieved Aug 2022

SOA FAM-L Exam Solutions: copy retrieved Aug 2022

Github repo and issues

# Uncomment next line to install package

# !pip install actuarialmath

"""Solutions code and hints for SOA FAM-L sample questions

MIT License. Copyright 2022-2023, Terence Lim

"""

import math

import pandas as pd

import matplotlib.pyplot as plt

import numpy as np

from actuarialmath import Interest

from actuarialmath import Life

from actuarialmath import Survival

from actuarialmath import Lifetime

from actuarialmath import Fractional

from actuarialmath import Insurance

from actuarialmath import Annuity

from actuarialmath import Premiums

from actuarialmath import PolicyValues, Contract

from actuarialmath import Reserves

from actuarialmath import Recursion

from actuarialmath import LifeTable

from actuarialmath import SULT

from actuarialmath import SelectLife

from actuarialmath import MortalityLaws, Beta, Uniform, Makeham, Gompertz

from actuarialmath import ConstantForce

from actuarialmath import ExtraRisk

from actuarialmath import Mthly

from actuarialmath import UDD

from actuarialmath import Woolhouse

Helper to compare computed answers to expected solutions

import time

class IsClose:

"""Helper class for testing and reporting if two values are close"""

def __init__(self, rel_tol : float = 0.01, score : bool = False,

verbose: bool = False):

self.den = self.num = 0

self.score = score # whether to count INCORRECTs instead of assert

self.verbose = verbose # whether to run silently

self.incorrect = [] # to keep list of messages for INCORRECT

self.tol = rel_tol

self.tic = time.time()

def __call__(self, solution, answer, question="", rel_tol=None):

"""Compare solution to answer within relative tolerance

Args:

solution (str | numeric) : gold label

answer (str | numeric) : computed answer

question (str) : label to associate with this test

rel_tol (float) : relative tolerance to be considered close

"""

if isinstance(solution, str):

isclose = (solution == answer)

else:

isclose = math.isclose(solution, answer, rel_tol=rel_tol or self.tol)

self.den += 1

self.num += isclose

msg = f"{question} {solution}: {answer}"

if self.verbose:

print("-----", msg, "[OK]" if isclose else "[INCORRECT]", "-----")

if not self.score:

assert isclose, msg

if not isclose:

self.incorrect.append(msg)

return isclose

def __str__(self):

"""Display cumulative score and errors"""

return f"Elapsed: {time.time()-self.tic:.1f} secs\n" \

+ f"Passed: {self.num}/{self.den}\n" + "\n".join(self.incorrect)

isclose = IsClose(0.01, score=False, verbose=True)

1 Tables#

These tables are provided in the FAM-L exam

Interest Functions at i=0.05

Normal Distribution Table

Standard Ultimate Life Table

but you actually do not need them here!

print("Interest Functions at i=0.05")

UDD.interest_frame()

Interest Functions at i=0.05

| i(m) | d(m) | i/i(m) | d/d(m) | alpha(m) | beta(m) | |

|---|---|---|---|---|---|---|

| 1 | 0.05000 | 0.04762 | 1.00000 | 1.00000 | 1.00000 | 0.00000 |

| 2 | 0.04939 | 0.04820 | 1.01235 | 0.98795 | 1.00015 | 0.25617 |

| 4 | 0.04909 | 0.04849 | 1.01856 | 0.98196 | 1.00019 | 0.38272 |

| 12 | 0.04889 | 0.04869 | 1.02271 | 0.97798 | 1.00020 | 0.46651 |

| 0 | 0.04879 | 0.04879 | 1.02480 | 0.97600 | 1.00020 | 0.50823 |

print("Values of z for selected values of Pr(Z<=z)")

print(Life.quantiles_frame().to_string(float_format=lambda x: f"{x:.3f}"))

Values of z for selected values of Pr(Z<=z)

z 0.842 1.036 1.282 1.645 1.960 2.326 2.576

Pr(Z<=z) 0.800 0.850 0.900 0.950 0.975 0.990 0.995

print("Standard Ultimate Life Table at i=0.05")

SULT().frame()

Standard Ultimate Life Table at i=0.05

| l_x | q_x | a_x | A_x | 2A_x | a_x:10 | A_x:10 | a_x:20 | A_x:20 | 5_E_x | 10_E_x | 20_E_x | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 20 | 100000.0 | 0.000250 | 19.9664 | 0.04922 | 0.00580 | 8.0991 | 0.61433 | 13.0559 | 0.37829 | 0.78252 | 0.61224 | 0.37440 |

| 21 | 99975.0 | 0.000253 | 19.9197 | 0.05144 | 0.00614 | 8.0990 | 0.61433 | 13.0551 | 0.37833 | 0.78250 | 0.61220 | 0.37429 |

| 22 | 99949.7 | 0.000257 | 19.8707 | 0.05378 | 0.00652 | 8.0988 | 0.61434 | 13.0541 | 0.37837 | 0.78248 | 0.61215 | 0.37417 |

| 23 | 99924.0 | 0.000262 | 19.8193 | 0.05622 | 0.00694 | 8.0986 | 0.61435 | 13.0531 | 0.37842 | 0.78245 | 0.61210 | 0.37404 |

| 24 | 99897.8 | 0.000267 | 19.7655 | 0.05879 | 0.00739 | 8.0983 | 0.61437 | 13.0519 | 0.37848 | 0.78243 | 0.61205 | 0.37390 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 96 | 17501.8 | 0.192887 | 3.5597 | 0.83049 | 0.69991 | 3.5356 | 0.83164 | 3.5597 | 0.83049 | 0.19872 | 0.01330 | 0.00000 |

| 97 | 14125.9 | 0.214030 | 3.3300 | 0.84143 | 0.71708 | 3.3159 | 0.84210 | 3.3300 | 0.84143 | 0.16765 | 0.00827 | 0.00000 |

| 98 | 11102.5 | 0.237134 | 3.1127 | 0.85177 | 0.73356 | 3.1050 | 0.85214 | 3.1127 | 0.85177 | 0.13850 | 0.00485 | 0.00000 |

| 99 | 8469.7 | 0.262294 | 2.9079 | 0.86153 | 0.74930 | 2.9039 | 0.86172 | 2.9079 | 0.86153 | 0.11173 | 0.00266 | 0.00000 |

| 100 | 6248.2 | 0.289584 | 2.7156 | 0.87068 | 0.76427 | 2.7137 | 0.87078 | 2.7156 | 0.87068 | 0.08777 | 0.00136 | 0.00000 |

81 rows × 12 columns

2 Survival models#

SOA Question 2.1 : (B) 2.5

You are given:

\(S_0(t) = \left(1 - \frac{t}{\omega} \right)^{\frac{1}{4}}, \quad 0 \le t \le \omega\)

\(\mu_{65} = \frac{1}{180} \)

Calculate \(e_{106}\), the curtate expectation of life at age 106.

hints:

derive formula for \(\mu\) from given survival function

solve for \(\omega\) given \(\mu_{65}\)

calculate \(e\) by summing survival probabilities

life = Lifetime()

def mu_from_l(omega): # first solve for omega, given mu_65 = 1/180

return life.set_survival(l=lambda x,s: (1 - (x+s)/omega)**0.25).mu_x(65)

omega = int(life.solve(mu_from_l, target=1/180, grid=100))

e = life.set_survival(l=lambda x,s:(1 - (x + s)/omega)**.25, maxage=omega)\

.e_x(106) # then solve expected lifetime from omega

isclose(2.5, e, question="Q2.1")

----- Q2.1 2.5: 2.4786080555423604 [OK] -----

True

SOA Question 2.2 : (D) 400

Scientists are searching for a vaccine for a disease. You are given:

100,000 lives age x are exposed to the disease

Future lifetimes are independent, except that the vaccine, if available, will be given to all at the end of year 1

The probability that the vaccine will be available is 0.2

For each life during year 1, \(q_x\) = 0.02

For each life during year 2, \(q_{x+1}\) = 0.01 if the vaccine has been given and \(q_{x+1}\) = 0.02 if it has not been given

Calculate the standard deviation of the number of survivors at the end of year 2.

hints:

calculate survival probabilities for the two scenarios

apply conditional variance formula (or mixed distribution)

p1 = (1. - 0.02) * (1. - 0.01) # 2_p_x if vaccine given

p2 = (1. - 0.02) * (1. - 0.02) # 2_p_x if vaccine not given

std = math.sqrt(Life.conditional_variance(p=.2, p1=p1, p2=p2, N=100000))

isclose(400, std, question="Q2.2")

----- Q2.2 400: 396.5914603215815 [OK] -----

True

SOA Question 2.3 : (A) 0.0483

You are given that mortality follows Gompertz Law with B = 0.00027 and c = 1.1.

Calculate \(f_{50}(10)\).

hints:

Derive formula for \(f\) given survival function

B, c = 0.00027, 1.1

S = lambda x,s,t: np.exp(-B * c**(x+s) * (c**t - 1)/np.log(c))

life = Survival().set_survival(S=S)

f = life.f_x(x=50, t=10)

isclose(0.0483, f, question="Q2.3")

----- Q2.3 0.0483: 0.04838918022351102 [OK] -----

True

SOA Question 2.4 : (E) 8.2

You are given \(_tq_0 = \frac{t^2}{10,000} \quad 0 < t < 100\). Calculate \(\overset{\circ}{e}_{75:\overline{10|}}\).

hints:

derive survival probability function \(_tp_x\) given \(_tq_0\)

compute \(\overset{\circ}{e}\) by integration

def q(t) : return (t**2)/10000. if t < 100 else 1.

e = Lifetime().set_survival(l=lambda x,s: 1 - q(x+s)).e_x(75, t=10, curtate=False)

isclose(8.2, e, question="Q2.4")

----- Q2.4 8.2: 8.20952380952381 [OK] -----

True

SOA Question 2.5 : (B) 37.1

You are given the following:

\(e_{40:20} = 18\)

\(e_{60} = 25\)

\(_{20}q_{40} = 0.2\)

\(q_{40} = 0.003\)

Calculate \(e_{41}\).

hints:

solve for \(e_{40}\) from limited lifetime formula

compute \(e_{41}\) using forward recursion

life = Recursion(verbose=True).set_e(25, x=60, curtate=True)\

.set_q(0.2, x=40, t=20)\

.set_q(0.003, x=40)\

.set_e(18, x=40, t=20, curtate=True)

e = life.e_x(41, curtate=True)

isclose(37.1, e, question="Q2.5")

----- Q2.5 37.1: 37.11434302908726 [OK] -----

True

SOA Question 2.6 : (C) 13.3

You are given the survival function:

\(S_0(x) = \left( 1 − \frac{x}{60} \right)^{\frac{1}{3}}, \quad 0 \le x \le 60\)

Calculate \(1000 \mu_{35}\).

hints:

derive force of mortality function \(\mu\) from given survival function

life = Survival().set_survival(l=lambda x,s: (1 - (x+s)/60)**(1/3))

mu = 1000 * life.mu_x(35)

isclose(13.3, mu, question="Q2.6")

----- Q2.6 13.3: 13.333333333333586 [OK] -----

True

SOA Question 2.7 : (B) 0.1477

You are given the following survival function of a newborn:

Calculate the probability that (30) dies within the next 20 years.

hints:

calculate from given survival function

l = lambda x,s: (1-((x+s)/250) if (x+s)<40 else 1-((x+s)/100)**2)

q = Survival().set_survival(l=l).q_x(30, t=20)

isclose(0.1477, q, question="Q2.7")

----- Q2.7 0.1477: 0.1477272727272727 [OK] -----

True

SOA Question 2.8 : (C) 0.94

In a population initially consisting of 75% females and 25% males, you are given:

For a female, the force of mortality is constant and equals \(\mu\)

For a male, the force of mortality is constant and equals 1.5 \(\mu\)

At the end of 20 years, the population is expected to consist of 85% females and 15% males

Calculate the probability that a female survives one year.

hints:

relate \(p_{male}\) and \(p_{female}\) through the common term \(\mu\) and the given proportions

def fun(mu): # Solve first for mu, given ratio of start and end proportions

male = Survival().set_survival(mu=lambda x,s: 1.5 * mu)

female = Survival().set_survival(mu=lambda x,s: mu)

return (75 * female.p_x(0, t=20)) / (25 * male.p_x(0, t=20))

mu = Survival.solve(fun, target=85/15, grid=0.5)

p = Survival().set_survival(mu=lambda x,s: mu).p_x(0, t=1)

isclose(0.94, p, question="Q2.8")

----- Q2.8 0.94: 0.9383813306903799 [OK] -----

True

3 Life tables and selection#

SOA Question 3.1 : (B) 117

You are given:

An excerpt from a select and ultimate life table with a select period of 3 years:

\(x\) |

\(\ell_{[ x ]}\) |

\(\ell_{[x]+1}\) |

\(\ell_{[x]+2}\) |

\(\ell_{x+3}\) |

\(x+3\) |

|---|---|---|---|---|---|

60 |

80,000 |

79,000 |

77,000 |

74,000 |

63 |

61 |

78,000 |

76,000 |

73,000 |

70,000 |

64 |

62 |

75,000 |

72,000 |

69,000 |

67,000 |

65 |

63 |

71,000 |

68,000 |

66,000 |

65,000 |

66 |

Deaths follow a constant force of mortality over each year of age

Calculate \(1000~ _{23}q_{[60] + 0.75}\).

hints:

interpolate with constant force of maturity

life = SelectLife().set_table(l={60: [80000, 79000, 77000, 74000],

61: [78000, 76000, 73000, 70000],

62: [75000, 72000, 69000, 67000],

63: [71000, 68000, 66000, 65000]})

q = 1000 * life.q_r(60, s=0, r=0.75, t=3, u=2)

isclose(117, q, question="Q3.1")

----- Q3.1 117: 116.7192429022082 [OK] -----

True

SOA Question 3.2 : (D) 14.7

You are given:

The following extract from a mortality table with a one-year select period:

\(x\) |

\(l_{[x]}\) |

\(d_{[x]}\) |

\(l_{x+1}\) |

\(x + 1\) |

|---|---|---|---|---|

65 |

1000 |

40 |

− |

66 |

66 |

955 |

45 |

− |

67 |

Deaths are uniformly distributed over each year of age

\(\overset{\circ}{e}_{[65]} = 15.0\)

Calculate \(\overset{\circ}{e}_{[66]}\).

hints:

UDD \(\Rightarrow \overset{\circ}{e}_{x} = e_x + 0.5\)

fill select table using curtate expectations

e_curtate = Fractional.e_approximate(e_complete=15)

life = SelectLife(udd=True).set_table(l={65: [1000, None,],

66: [955, None]},

e={65: [e_curtate, None]},

d={65: [40, None,],

66: [45, None]})

e = life.e_r(x=66)

isclose(14.7, e, question="Q3.2")

----- Q3.2 14.7: 14.67801047120419 [OK] -----

True

SOA Question 3.3 : (E) 1074

You are given:

An excerpt from a select and ultimate life table with a select period of 2 years:

\(x\) |

\(\ell_{[ x ]}\) |

\(\ell_{[ x ] + 1}\) |

\(\ell_{x + 2}\) |

\(x + 2\) |

|---|---|---|---|---|

50 |

99,000 |

96,000 |

93,000 |

52 |

51 |

97,000 |

93,000 |

89,000 |

53 |

52 |

93,000 |

88,000 |

83,000 |

54 |

53 |

90,000 |

84,000 |

78,000 |

55 |

Deaths are uniformly distributed over each year of age

Calculate \(10,000 ~ _{2.2}q_{[51]+0.5}\).

hints:

interpolate lives between integer ages with UDD

life = SelectLife().set_table(l={50: [99, 96, 93],

51: [97, 93, 89],

52: [93, 88, 83],

53: [90, 84, 78]})

q = 10000 * life.q_r(51, s=0, r=0.5, t=2.2)

isclose(1074, q, question="Q3.3")

----- Q3.3 1074: 1073.684210526316 [OK] -----

True

SOA Question 3.4 : (B) 815

The SULT Club has 4000 members all age 25 with independent future lifetimes. The mortality for each member follows the Standard Ultimate Life Table.

Calculate the largest integer N, using the normal approximation, such that the probability that there are at least N survivors at age 95 is at least 90%.

hints:

compute portfolio percentile with N=4000, and mean and variance from binomial distribution

sult = SULT()

mean = sult.p_x(25, t=95-25)

var = sult.bernoulli(mean, variance=True)

pct = sult.portfolio_percentile(N=4000, mean=mean, variance=var, prob=0.1)

isclose(815, pct, question="Q3.4")

----- Q3.4 815: 815.0943255167722 [OK] -----

True

SOA Question 3.5 : (E) 106

You are given:

\(x\) |

60 |

61 |

62 |

63 |

64 |

65 |

66 |

67 |

|---|---|---|---|---|---|---|---|---|

\(l_x\) |

99,999 |

88,888 |

77,777 |

66,666 |

55,555 |

44,444 |

33,333 |

22,222 |

\(a =~ _{3.4|2.5}q_{60}\) assuming a uniform distribution of deaths over each year of age

\(b =~ _{3.4|2.5}q_{60}\) assuming a constant force of mortality over each year of age

Calculate \(100,000( a − b )\)

hints:

compute mortality rates by interpolating lives between integer ages, with UDD and constant force of mortality assumptions

l = [99999, 88888, 77777, 66666, 55555, 44444, 33333, 22222]

a = LifeTable(udd=True).set_table(l={age:l for age,l in zip(range(60, 68), l)})\

.q_r(60, u=3.4, t=2.5)

b = LifeTable(udd=False).set_table(l={age:l for age,l in zip(range(60, 68), l)})\

.q_r(60, u=3.4, t=2.5)

isclose(106, 100000 * (a - b), question="Q3.5")

----- Q3.5 106: 106.16575827938624 [OK] -----

True

SOA Question 3.6 : (D) 15.85

You are given the following extract from a table with a 3-year select period:

\(x\) |

\(q_{[x]}\) |

\(q_{[x]+1}\) |

\(q_{[x]+2}\) |

\(q_{x+3}\) |

\(x+3\) |

|---|---|---|---|---|---|

60 |

0.09 |

0.11 |

0.13 |

0.15 |

63 |

61 |

0.10 |

0.12 |

0.14 |

0.16 |

64 |

62 |

0.11 |

0.13 |

0.15 |

0.17 |

65 |

63 |

0.12 |

0.14 |

0.16 |

0.18 |

66 |

64 |

0.13 |

0.15 |

0.17 |

0.19 |

67 |

\(e_{64} = 5.10\)

Calculate \(e_{[61]}\).

hints:

apply recursion formulas for curtate expectation

e = SelectLife().set_table(q={60: [.09, .11, .13, .15],

61: [.1, .12, .14, .16],

62: [.11, .13, .15, .17],

63: [.12, .14, .16, .18],

64: [.13, .15, .17, .19]},

e={61: [None, None, None, 5.1]})\

.e_x(61)

isclose(5.85, e, question="Q3.6")

----- Q3.6 5.85: 5.846832 [OK] -----

True

SOA Question 3.7 : (b) 16.4

For a mortality table with a select period of two years, you are given:

\(x\) |

\(q_{[x]}\) |

\(q_{[x]+1}\) |

\(q_{x+2}\) |

\(x+2\) |

|---|---|---|---|---|

50 |

0.0050 |

0.0063 |

0.0080 |

52 |

51 |

0.0060 |

0.0073 |

0.0090 |

53 |

52 |

0.0070 |

0.0083 |

0.0100 |

54 |

53 |

0.0080 |

0.0093 |

0.0110 |

55 |

The force of mortality is constant between integral ages.

Calculate \(1000 ~_{2.5}q_{[50]+0.4}\).

hints:

use deferred mortality formula

use chain rule for survival probabilities,

interpolate between integer ages with constant force of mortality

life = SelectLife().set_table(q={50: [.0050, .0063, .0080],

51: [.0060, .0073, .0090],

52: [.0070, .0083, .0100],

53: [.0080, .0093, .0110]})

q = 1000 * life.q_r(50, s=0, r=0.4, t=2.5)

isclose(16.4, q, question="Q3.7")

----- Q3.7 16.4: 16.420207214428586 [OK] -----

True

SOA Question 3.8 : (B) 1505

A club is established with 2000 members, 1000 of exact age 35 and 1000 of exact age 45. You are given:

Mortality follows the Standard Ultimate Life Table

Future lifetimes are independent

N is the random variable for the number of members still alive 40 years after the club is established

Using the normal approximation, without the continuity correction, calculate the smallest \(n\) such that \(Pr( N \ge n ) \le 0.05\).

hints:

compute portfolio means and variances from sum of 2000 independent members’ means and variances of survival.

sult = SULT()

p1 = sult.p_x(35, t=40)

p2 = sult.p_x(45, t=40)

mean = sult.bernoulli(p1) * 1000 + sult.bernoulli(p2) * 1000

var = (sult.bernoulli(p1, variance=True) * 1000

+ sult.bernoulli(p2, variance=True) * 1000)

pct = sult.portfolio_percentile(mean=mean, variance=var, prob=.95)

isclose(1505, pct, question="Q3.8")

----- Q3.8 1505: 1504.8328375406456 [OK] -----

True

SOA Question 3.9 : (E) 3850

A father-son club has 4000 members, 2000 of which are age 20 and the other 2000 are age 45. In 25 years, the members of the club intend to hold a reunion.

You are given:

All lives have independent future lifetimes.

Mortality follows the Standard Ultimate Life Table.

Using the normal approximation, without the continuity correction, calculate the 99th percentile of the number of surviving members at the time of the reunion.

hints:

compute portfolio means and variances as sum of 4000 independent members’ means and variances (of survival)

retrieve normal percentile

sult = SULT()

p1 = sult.p_x(20, t=25)

p2 = sult.p_x(45, t=25)

mean = sult.bernoulli(p1) * 2000 + sult.bernoulli(p2) * 2000

var = (sult.bernoulli(p1, variance=True) * 2000

+ sult.bernoulli(p2, variance=True) * 2000)

pct = sult.portfolio_percentile(mean=mean, variance=var, prob=.99)

isclose(3850, pct, question="Q3.9")

----- Q3.9 3850: 3850.144345130047 [OK] -----

True

SOA Question 3.10 : (C) 0.86

A group of 100 people start a Scissor Usage Support Group. The rate at which members enter and leave the group is dependent on whether they are right-handed or left-handed.

You are given the following:

The initial membership is made up of 75% left-handed members (L) and 25% right-handed members (R)

After the group initially forms, 35 new (L) and 15 new (R) join the group at the start of each subsequent year

Members leave the group only at the end of each year

\(q_L\) = 0.25 for all years

\(q_R\) = 0.50 for all years

Calculate the proportion of the Scissor Usage Support Group’s expected membership that is left-handed at the start of the group’s 6th year, before any new members join for that year.

hints:

reformulate the problem by reversing time: survival to year 6 is calculated in reverse as discounting by the same number of years.

interest = Interest(v=0.75)

L = 35*interest.annuity(t=4, due=False) + 75*interest.v_t(t=5)

interest = Interest(v=0.5)

R = 15*interest.annuity(t=4, due=False) + 25*interest.v_t(t=5)

isclose(0.86, L / (L + R), question="Q3.10")

----- Q3.10 0.86: 0.8578442833761983 [OK] -----

True

SOA Question 3.11 : (B) 0.03

For the country of Bienna, you are given:

Bienna publishes mortality rates in biennial form, that is, mortality rates are of the form: \(_2q_{2x},\) for \(x = 0,1, 2,...\)

Deaths are assumed to be uniformly distributed between ages \(2x\) and \(2x + 2\), for \(x = 0,1, 2,...\)

\(_2q_{50} = 0.02\)

\(_2q_{52} = 0.04\)

Calculate the probability that (50) dies during the next 2.5 years.

hints:

calculate mortality rate by interpolating lives assuming UDD

life = LifeTable(udd=True).set_table(q={50//2: .02, 52//2: .04})

q = life.q_r(50//2, t=2.5/2)

isclose(0.03, q, question="Q3.11")

----- Q3.11 0.03: 0.0298 [OK] -----

True

SOA Question 3.12 : (C) 0.055

X and Y are both age 61. X has just purchased a whole life insurance policy. Y purchased a whole life insurance policy one year ago.

Both X and Y are subject to the following 3-year select and ultimate table:

\(x\) |

\(\ell_{[x]}\) |

\(\ell_{[x]+1}\) |

\(\ell_{[x] + 2}\) |

\(\ell_{x+3}\) |

\(x+3\) |

|---|---|---|---|---|---|

60 |

10,000 |

9,600 |

8,640 |

7,771 |

63 |

61 |

8,654 |

8,135 |

6,996 |

5,737 |

64 |

62 |

7,119 |

6,549 |

5,501 |

4,016 |

65 |

63 |

5,760 |

4,954 |

3,765 |

2,410 |

66 |

The force of mortality is constant over each year of age.

Calculate the difference in the probability of survival to age 64.5 between X and Y.

hints:

compute survival probability by interpolating lives assuming constant force

life = SelectLife(udd=False).set_table(l={60: [10000, 9600, 8640, 7771],

61: [8654, 8135, 6996, 5737],

62: [7119, 6549, 5501, 4016],

63: [5760, 4954, 3765, 2410]})

q = life.q_r(60, s=1, t=3.5) - life.q_r(61, s=0, t=3.5)

isclose(0.055, q, question="Q3.12")

----- Q3.12 0.055: 0.05465655938591829 [OK] -----

True

SOA Question 3.13 : (B) 1.6

A life is subject to the following 3-year select and ultimate table:

\([x]\) |

\(\ell_{[x]}\) |

\(\ell_{[x]+1}\) |

\(\ell_{[x]+2}\) |

\(\ell_{x+3}\) |

\(x+3\) |

|---|---|---|---|---|---|

55 |

10,000 |

9,493 |

8,533 |

7,664 |

58 |

56 |

8,547 |

8,028 |

6,889 |

5,630 |

59 |

57 |

7,011 |

6,443 |

5,395 |

3,904 |

60 |

58 |

5,853 |

4,846 |

3,548 |

2,210 |

61 |

You are also given:

\(e_{60} = 1\)

Deaths are uniformly distributed over each year of age

Calculate \(\overset{\circ}{e}_{[58]+2}\) .

hints:

compute curtate expectations using recursion formulas

convert to complete expectation assuming UDD

life = SelectLife().set_table(l={55: [10000, 9493, 8533, 7664],

56: [8547, 8028, 6889, 5630],

57: [7011, 6443, 5395, 3904],

58: [5853, 4846, 3548, 2210]},

e={57: [None, None, None, 1]})

e = life.e_r(x=58, s=2)

isclose(1.6, e, question="Q3.13")

----- Q3.13 1.6: 1.6003382187147688 [OK] -----

True

SOA Question 3.14 : (C) 0.345

You are given the following information from a life table:

x |

\(l_x\) |

\(d_x\) |

\(p_x\) |

\(q_x\) |

|---|---|---|---|---|

95 |

− |

− |

− |

0.40 |

96 |

− |

− |

0.20 |

− |

97 |

− |

72 |

− |

1.00 |

You are also given:

\(l_{90} = 1000\) and \(l_{93} = 825\)

Deaths are uniformly distributed over each year of age.

Calculate the probability that (90) dies between ages 93 and 95.5.

hints:

compute mortality by interpolating lives between integer ages assuming UDD

life = LifeTable(udd=True).set_table(l={90: 1000, 93: 825},

d={97: 72},

p={96: .2},

q={95: .4, 97: 1})

q = life.q_r(90, u=93-90, t=95.5 - 93)

isclose(0.345, q, question="Q3.14")

----- Q3.14 0.345: 0.345 [OK] -----

True

4 Insurance benefits#

SOA Question 4.1 : (A) 0.27212

For a special whole life insurance policy issued on (40), you are given:

Death benefits are payable at the end of the year of death

The amount of benefit is 2 if death occurs within the first 20 years and is 1 thereafter

Z is the present value random variable for the payments under this insurance

i = 0.03

x |

\(A_x\) |

\(_{20}E_x\) |

|---|---|---|

40 |

0.36987 |

0.51276 |

60 |

0.62567 |

0.17878 |

\(E[Z^2] =0.24954\)

Calculate the standard deviation of Z.

hints:

solve EPV as sum of term and deferred insurance

compute variance as difference of second moment and first moment squared

life = Recursion().set_interest(i=0.03)

life.set_A(0.36987, x=40).set_A(0.62567, x=60)

life.set_E(0.51276, x=40, t=20).set_E(0.17878, x=60, t=20)

Z2 = 0.24954

A = (2 * life.term_insurance(40, t=20) + life.deferred_insurance(40, u=20))

std = math.sqrt(life.insurance_variance(A2=Z2, A1=A))

isclose(0.27212, std, question="Q4.1")

----- Q4.1 0.27212: 0.2721117749374753 [OK] -----

True

SOA Question 4.2 : (D) 0.18

or a special 2-year term insurance policy on (x), you are given:

Death benefits are payable at the end of the half-year of death

The amount of the death benefit is 300,000 for the first half-year and increases by 30,000 per half-year thereafter

\(q_x\) = 0.16 and \(q_{x+1}\) = 0.23

\(i^{(2)}\) = 0.18

Deaths are assumed to follow a constant force of mortality between integral ages

Z is the present value random variable for this insurance

Calculate Pr( Z > 277,000) .

hints:

calculate Z(t) and deferred mortality for each half-yearly t

sum the deferred mortality probabilities for periods when PV > 277000

life = LifeTable(udd=False).set_table(q={0: .16, 1: .23})\

.set_interest(i_m=.18, m=2)

mthly = Mthly(m=2, life=life)

Z = mthly.Z_m(0, t=2, benefit=lambda x,t: 300000 + t*30000*2)

p = Z[Z['Z'] >= 277000]['q'].sum()

isclose(0.18, p, question="Q4.2")

----- Q4.2 0.18: 0.17941813045022975 [OK] -----

True

SOA Question 4.3 : (D) 0.878

You are given:

\(q_{60} = 0.01\)

Using \(i = 0.05, ~ A_{60:\overline{3|}} = 0.86545\)

Using \(i = 0.045\) calculate \(A_{60:\overline{3|}}\)

hints:

solve \(q_{61}\) from endowment insurance EPV formula

solve \(A_{60:\overline{3|}}\) with new \(i=0.045\) as EPV of endowment insurance benefits.

life = Recursion(verbose=True).set_interest(i=0.05)\

.set_q(0.01, x=60)\

.set_A(0.86545, x=60, t=3, endowment=1)

q = life.q_x(x=61)

A = Recursion(verbose=True).set_interest(i=0.045)\

.set_q(0.01, x=60)\

.set_q(q, x=61)\

.endowment_insurance(60, t=3)

isclose(0.878, A, question="Q4.3")

----- Q4.3 0.878: 0.8777667236003878 [OK] -----

True

SOA Question 4.4 : (A) 0.036

For a special increasing whole life insurance on (40), payable at the moment of death, you are given :

The death benefit at time t is \(b_t = 1 + 0.2 t, \quad t \ge 0\)

The interest discount factor at time t is \(v(t) = (1 + 0.2 t ) − 2, \quad t \ge 0\)

\(_tp_{40} ~ \mu_{40+t} = 0.025~\text{if} ~ 0 \le t < 40\), otherwise \(0\)

Z is the present value random variable for this insurance

Calculate Var(Z).

hints:

integrate to find EPV of \(Z\) and \(Z^2\)

variance is difference of second moment and first moment squared

x = 40

life = Insurance().set_survival(f=lambda *x: 0.025, maxage=x+40)\

.set_interest(v_t=lambda t: (1 + .2*t)**(-2))

def benefit(x,t): return 1 + .2 * t

A1 = life.A_x(x, benefit=benefit, discrete=False)

A2 = life.A_x(x, moment=2, benefit=benefit, discrete=False)

var = A2 - A1**2

isclose(0.036, var, question="Q4.4")

----- Q4.4 0.036: 0.03567680106032681 [OK] -----

True

SOA Question 4.5 : (C) 35200

For a 30-year term life insurance of 100,000 on (45), you are given:

The death benefit is payable at the moment of death

Mortality follows the Standard Ultimate Life Table

\(\delta = 0.05\)

Deaths are uniformly distributed over each year of age

Calculate the 95th percentile of the present value of benefits random variable for this insurance

hints:

interpolate between integer ages with UDD, and find lifetime that mortality rate exceeded

compute PV of death benefit paid at that time.

sult = SULT(udd=True).set_interest(delta=0.05)

Z = 100000 * sult.Z_from_prob(45, prob=0.95, discrete=False)

isclose(35200, Z, question="Q4.5")

----- Q4.5 35200: 35187.95203719652 [OK] -----

True

SOA Question 4.6 : (B) 29.85

For a 3-year term insurance of 1000 on (70), you are given:

\(q^{SULT}_{70+k}\) is the mortality rate from the Standard Ultimate Life Table, for k = 0,1,2

\(q_{70 + k}\) is the mortality rate used to price this insurance, for k = 0,1, 2

\(q_{70 + k} = (0.95)^k q_{70+k}^{SULT}\), for k = 0,1, 2

i = 0.05

Calculate the single net premium.

hints:

calculate adjusted mortality rates

compute term insurance as EPV of benefits

sult = SULT()

life = LifeTable().set_interest(i=0.05)\

.set_table(q={70+k: .95**k * sult.q_x(70+k) for k in range(3)})

A = life.term_insurance(70, t=3, b=1000)

isclose(29.85, A, question="Q4.6")

----- Q4.6 29.85: 29.848351103559015 [OK] -----

True

SOA Question 4.7 : (B) 0.06

For a 25-year pure endowment of 1 on (x), you are given:

Z is the present value random variable at issue of the benefit payment

Var (Z) = 0.10 E[Z]

\(_{25}p_x = 0.57\)

Calculate the annual effective interest rate.

hints:

use Bernoulli shortcut formula for variance of pure endowment Z

solve for \(i\), since \(p\) is given.

def fun(i):

life = Recursion(verbose=False).set_interest(i=i)\

.set_p(0.57, x=0, t=25)

return 0.1*life.E_x(0, t=25) - life.E_x(0, t=25, moment=life.VARIANCE)

i = Recursion.solve(fun, target=0, grid=[0.058, 0.066])

isclose(0.06, i, question="Q4.7")

----- Q4.7 0.06: 0.06008023738770257 [OK] -----

True

SOA Question 4.8 : (C) 191

For a whole life insurance of 1000 on (50), you are given :

The death benefit is payable at the end of the year of death

Mortality follows the Standard Ultimate Life Table

i = 0.04 in the first year, and i = 0.05 in subsequent years

Calculate the actuarial present value of this insurance.

hints:

use insurance recursion with special interest rate \(i=0.04\) in first year.

def v_t(t): return 1.04**(-t) if t < 1 else 1.04**(-1) * 1.05**(-t+1)

A = SULT().set_interest(v_t=v_t).whole_life_insurance(50, b=1000)

isclose(191, A, question="Q4.8")

----- Q4.8 191: 191.12812818823548 [OK] -----

True

SOA Question 4.9 : (D) 0.5

You are given:

\(A_{35:\overline{15|}} = 0.39\)

\(A^1_{35:\overline{15|}} = 0.25\)

\(A_{35} = 0.32\)

Calculate \(A_{50}\).

hints:

solve \(_{15}E_{35}\) from endowment insurance minus term insurance

solve implicitly from whole life as term plus deferred insurance

E = Recursion().set_A(0.39, x=35, t=15, endowment=1)\

.set_A(0.25, x=35, t=15)\

.E_x(35, t=15)

life = Recursion(verbose=False).set_A(0.32, x=35)\

.set_E(E, x=35, t=15)

def fun(A): return life.set_A(A, x=50).term_insurance(35, t=15)

A = life.solve(fun, target=0.25, grid=[0.35, 0.55])

isclose(0.5, A, question="Q4.9")

----- Q4.9 0.5: 0.5 [OK] -----

True

SOA Question 4.10 : (D)

The present value random variable for an insurance policy on (x) is expressed as: $\(\begin{align*} Z & =0, \quad \textrm{if } T_x \le 10\\ & =v^T, \quad \textrm{if } 10 < T_x \le 20\\ & =2v^T, \quad \textrm{if } 20 < T_x \le 30\\ & =0, \quad \textrm{thereafter} \end{align*}\)$

Determine which of the following is a correct expression for \(E[Z]\).

(A) \(_{10|}\overline{A}_x + _{20|}\overline{A}_x - _{30|}\overline{A}_x\)

(B) \(\overline{A}_x + _{20}E_x \overline{A}_{x+20} - 2~_{30}E_x \overline{A}_{x +30}\)

(C) \(_{10}E_x \overline{A}_x + _{20}E_x \overline{A}_{x+20} - 2 ~_{30}E_x \overline{A}_{x +30}\)

(D) \(_{10}E_x \overline{A}_{x+10} + _{20}E_x \overline{A}_{x+20} - 2~ _{30}E_x \overline{A}_{x+30}\)

(E) \(_{10}E_x [\overline{A}_{x} + _{10}E_{x+10} + \overline{A}_{x+20} - _{10}E_{x+20} + \overline{A}_{x+30}]\)

hints:

draw and compare benefit diagrams

life = Insurance().set_interest(i=0.0).set_survival(S=lambda x,s,t: 1, maxage=40)

def fun(x, t):

if 10 <= t <= 20: return life.interest.v_t(t)

elif 20 < t <= 30: return 2 * life.interest.v_t(t)

else: return 0

def A(x, t): # Z_x+k (t-k)

return life.interest.v_t(t - x) * (t > x)

x = 0

benefits=[lambda x,t: (life.E_x(x, t=10) * A(x+10, t)

+ life.E_x(x, t=20)* A(x+20, t)

- life.E_x(x, t=30) * A(x+30, t)),

lambda x,t: (A(x, t)

+ life.E_x(x, t=20) * A(x+20, t)

- 2 * life.E_x(x, t=30) * A(x+30, t)),

lambda x,t: (life.E_x(x, t=10) * A(x, t)

+ life.E_x(x, t=20) * A(x+20, t)

- 2 * life.E_x(x, t=30) * A(x+30, t)),

lambda x,t: (life.E_x(x, t=10) * A(x+10, t)

+ life.E_x(x, t=20) * A(x+20, t)

- 2 * life.E_x(x, t=30) * A(x+30, t)),

lambda x,t: (life.E_x(x, t=10)

* (A(x+10, t)

+ life.E_x(x+10, t=10) * A(x+20, t)

- life.E_x(x+20, t=10) * A(x+30, t)))]

fig, ax = plt.subplots(3, 2)

ax = ax.ravel()

for i, b in enumerate([fun] + benefits):

life.Z_plot(0, benefit=b, ax=ax[i], color=f"C{i+1}", title='')

ax[i].legend(["(" + "abcde"[i-1] + ")" if i else "Z"])

z = [sum(abs(b(0, t) - fun(0, t)) for t in range(40)) for b in benefits]

ans = "ABCDE"[np.argmin(z)]

isclose('D', ans, question="Q4.10")

----- Q4.10 D: D [OK] -----

True

SOA Question 4.11 : (A) 143385

You are given:

\(Z_1\) is the present value random variable for an n-year term insurance of 1000 issued to (x)

\(Z_2\) is the present value random variable for an n-year endowment insurance of 1000 issued to (x)

For both \(Z_1\) and \(Z_2\) the death benefit is payable at the end of the year of death

\(E [ Z_1 ] = 528\)

\(Var ( Z_2 ) = 15,000\)

\(A^{~~~~1}_{x:{\overline{n|}}} = 0.209\)

\(^2A^{~~~~1}_{x:{\overline{n|}}} = 0.136\)

Calculate \(Var(Z_1)\).

hints:

compute endowment insurance = term insurance + pure endowment

apply formula of variance as the difference of second moment and first moment squared.

A1 = 528/1000 # E[Z1] term insurance

C1 = 0.209 # E[pure_endowment]

C2 = 0.136 # E[pure_endowment^2]

B1 = A1 + C1 # endowment = term + pure_endowment

def fun(A2):

B2 = A2 + C2 # double force of interest

return Insurance.insurance_variance(A2=B2, A1=B1)

A2 = Insurance.solve(fun, target=15000/(1000*1000), grid=[143400, 279300])

var = Insurance.insurance_variance(A2=A2, A1=A1, b=1000)

isclose(143385, var, question="Q4.11")

----- Q4.11 143385: 143384.99999999997 [OK] -----

True

SOA Question 4.12 : (C) 167

For three fully discrete insurance products on the same (x), you are given:

\(Z_1\) is the present value random variable for a 20-year term insurance of 50

\(Z_2\) is the present value random variable for a 20-year deferred whole life insurance of 100

\(Z_3\) is the present value random variable for a whole life insurance of 100.

\(E[Z_1] = 1.65\) and \(E[Z_2] = 10.75\)

\(Var(Z_1) = 46.75\) and \(Var(Z_2) = 50.78\)

Calculate \(Var(Z_3)\).

hints:

since \(Z_1,~Z_2\) are non-overlapping, \(E[Z_1~ Z_2] = 0\) for computing \(Cov(Z_1, Z_2)\)

whole life is sum of term and deferred, hence equals variance of components plus twice their covariance

cov = Life.covariance(a=1.65, b=10.75, ab=0) # E[Z1 Z2] = 0 nonoverlapping

var = Life.variance(a=2, b=1, var_a=46.75, var_b=50.78, cov_ab=cov)

isclose(167, var, question="Q4.12")

----- Q4.12 167: 166.82999999999998 [OK] -----

True

SOA Question 4.13 : (C) 350

For a 2-year deferred, 2-year term insurance of 2000 on [65], you are given:

The following select and ultimate mortality table with a 3-year select period:

\(x\) |

\(q_{[x]}\) |

\(q_{[x]+1}\) |

\(q_{[x]+2}\) |

\(q_{x+3}\) |

\(x+3\) |

|---|---|---|---|---|---|

65 |

0.08 |

0.10 |

0.12 |

0.14 |

68 |

66 |

0.09 |

0.11 |

0.13 |

0.15 |

69 |

67 |

0.10 |

0.12 |

0.14 |

0.16 |

70 |

68 |

0.11 |

0.13 |

0.15 |

0.17 |

71 |

69 |

0.12 |

0.14 |

0.16 |

0.18 |

72 |

\(i = 0.04\)

The death benefit is payable at the end of the year of death

Calculate the actuarial present value of this insurance.

hints:

compute term insurance as EPV of benefits

life = SelectLife().set_table(q={65: [.08, .10, .12, .14],

66: [.09, .11, .13, .15],

67: [.10, .12, .14, .16],

68: [.11, .13, .15, .17],

69: [.12, .14, .16, .18]})\

.set_interest(i=.04)

A = life.deferred_insurance(65, t=2, u=2, b=2000)

isclose(350, A, question="Q4.13")

----- Q4.13 350: 351.0578236056159 [OK] -----

True

SOA Question 4.14 : (E) 390000

A fund is established for the benefit of 400 workers all age 60 with independent future lifetimes. When they reach age 85, the fund will be dissolved and distributed to the survivors.

The fund will earn interest at a rate of 5% per year.

The initial fund balance, \(F\), is determined so that the probability that the fund will pay at least 5000 to each survivor is 86%, using the normal approximation.

Mortality follows the Standard Ultimate Life Table.

Calculate \(F\).

hints:

discount (by interest rate \(i=0.05\)) the value at the portfolio percentile, of the sum of 400 bernoulli r.v. with survival probability \(_{25}p_{60}\)

sult = SULT()

p = sult.p_x(60, t=85-60)

mean = sult.bernoulli(p)

var = sult.bernoulli(p, variance=True)

F = sult.portfolio_percentile(mean=mean, variance=var, prob=.86, N=400)

F *= 5000 * sult.interest.v_t(85-60)

isclose(390000, F, question="Q4.14")

----- Q4.14 390000: 389322.86778416135 [OK] -----

True

SOA Question 4.15 : (E) 0.0833

For a special whole life insurance on (x), you are given :

Death benefits are payable at the moment of death

The death benefit at time \(t\) is \(b_t = e^{0.02t}\), for \(t \ge 0\)

\(\mu_{x+t} = 0.04\), for \(t \ge 0\)

\(\delta = 0.06\)

Z is the present value at issue random variable for this insurance.

Calculate \(Var(Z)\).

hints:

this special benefit function has effect of reducing actuarial discount rate to use in constant force of mortality shortcut formulas

life = Insurance().set_survival(mu=lambda *x: 0.04).set_interest(delta=0.06)

benefit = lambda x,t: math.exp(0.02*t)

A1 = life.A_x(0, benefit=benefit, discrete=False)

A2 = life.A_x(0, moment=2, benefit=benefit, discrete=False)

var = life.insurance_variance(A2=A2, A1=A1)

isclose(0.0833, var, question="Q4.15")

----- Q4.15 0.0833: 0.08333333333333331 [OK] -----

True

SOA Question 4.16 : (D) 0.11

You are given the following extract of ultimate mortality rates from a two-year select and ultimate mortality table:

\(x\) |

\(q_x\) |

|---|---|

50 |

0.045 |

51 |

0.050 |

52 |

0.055 |

53 |

0.060 |

The select mortality rates satisfy the following:

\(q_{[x]} = 0.7 q_x\)

\(q_{[x]+1} = 0.8 q_{x + 1}\)

You are also given that \(i = 0.04\).

Calculate \(A^1_{[50]:\overline{3|}}\).

hints:

compute EPV of future benefits with adjusted mortality rates

q = [.045, .050, .055, .060]

q = {50 + x: [q[x] * 0.7 if x < len(q) else None,

q[x+1] * 0.8 if x + 1 < len(q) else None,

q[x+2] if x + 2 < len(q) else None]

for x in range(4)}

life = SelectLife().set_table(q=q).set_interest(i=.04)

A = life.term_insurance(50, t=3)

isclose(0.1116, A, question="Q4.16")

----- Q4.16 0.1116: 0.1115661982248521 [OK] -----

True

SOA Question 4.17 : (A) 1126.7

For a special whole life policy on (48), you are given:

The policy pays 5000 if the insured’s death is before the median curtate future lifetime at issue and 10,000 if death is after the median curtate future lifetime at issue

Mortality follows the Standard Ultimate Life Table

Death benefits are paid at the end of the year of death

i = 0.05

Calculate the actuarial present value of benefits for this policy.

hints:

find future lifetime with 50% survival probability

compute EPV of special whole life as sum of term and deferred insurance, that have different benefit amounts before and after median lifetime.

sult = SULT()

median = sult.Z_t(48, prob=0.5, discrete=False)

def benefit(x,t): return 5000 if t < median else 10000

A = sult.A_x(48, benefit=benefit)

isclose(1130, A, question="Q4.17")

----- Q4.17 1130: 1126.7747728948445 [OK] -----

True

SOA Question 4.18 : (A) 81873

You are given that T, the time to first failure of an industrial robot, has a density f(t) given by

with \(f(t)\) undetermined on \([10, \infty)\).

Consider a supplemental warranty on this robot that pays 100,000 at the time T of its first failure if \(2 \le T \le 10\) , with no benefits payable otherwise. You are also given that \(\delta = 5\%\). Calculate the 90th percentile of the present value of the future benefits under this warranty.

hints:

find values of limits such that integral of lifetime density function equals required survival probability

def f(x,s,t): return 0.1 if t < 2 else 0.4*t**(-2)

life = Insurance().set_interest(delta=0.05)\

.set_survival(f=f, maxage=10)

def benefit(x,t): return 0 if t < 2 else 100000

prob = 0.9 - life.q_x(0, t=2)

T = life.Z_t(0, prob=prob)

Z = life.Z_from_t(T, discrete=False) * benefit(0, T)

isclose(81873, Z, question="Q4.18")

----- Q4.18 81873: 81873.07530779815 [OK] -----

True

SOA Question 4.19 : (B) 59050

(80) purchases a whole life insurance policy of 100,000. You are given:

The policy is priced with a select period of one year

The select mortality rate equals 80% of the mortality rate from the Standard Ultimate Life Table

Ultimate mortality follows the Standard Ultimate Life Table

\(i = 0.05\)

Calculate the actuarial present value of the death benefits for this insurance

hints:

calculate adjusted mortality for the one-year select period

compute whole life insurance using backward recursion formula

life = SULT()

q = ExtraRisk(life=life, extra=0.8, risk="MULTIPLY_RATE")['q']

select = SelectLife(periods=1).set_select(s=0, age_selected=True, q=q)\

.set_select(s=1, age_selected=False, q=life['q'])\

.set_interest(i=.05)\

.fill_table()

A = 100000 * select.whole_life_insurance(80, s=0)

isclose(59050, A, question="Q4.19")

----- Q4.19 59050: 59050.59973285648 [OK] -----

True

5 Annuities#

SOA Question 5.1 : (A) 0.705

You are given:

\(\delta_t = 0.06, \quad t \ge 0\)

\(\mu_x(t) = 0.01, \quad t \ge 0\)

\(Y\) is the present value random variable for a continuous annuity of 1 per year, payable for the lifetime of (x) with 10 years certain

Calculate \(Pr( Y > E[Y])\).

hints:

sum annuity certain and deferred life annuity with constant force of mortality shortcut

apply equation for PV annuity r.v. Y to infer lifetime

compute survival probability from constant force of mortality function.

life = ConstantForce(mu=0.01).set_interest(delta=0.06)

EY = life.certain_life_annuity(0, u=10, discrete=False)

p = life.p_x(0, t=life.Y_to_t(EY))

isclose(0.705, p, question="Q5.1") # 0.705

----- Q5.1 0.705: 0.7053680433746505 [OK] -----

True

SOA Question 5.2 : (B) 9.64

You are given:

\(A_x = 0.30\)

\(A_{x + n} = 0.40\)

\(A^{~~~~1}_{x:\overline{n|}} = 0.35\)

i = 0.05

Calculate \(a_{x:\overline{n|}}\).

hints:

compute term life as difference of whole life and deferred insurance

compute twin annuity-due, and adjust to an immediate annuity.

x, n = 0, 10

a = Recursion().set_interest(i=0.05)\

.set_A(0.3, x)\

.set_A(0.4, x+n)\

.set_E(0.35, x, t=n)\

.immediate_annuity(x, t=n)

isclose(9.64, a, question="Q5.2")

----- Q5.2 9.64: 9.639999999999999 [OK] -----

True

SOA Question 5.3 : (C) 6.239

You are given:

Mortality follows the Standard Ultimate Life Table

Deaths are uniformly distributed over each year of age

i = 0.05

Calculate \(\frac{d}{dt}(\overline{I}\overline{a})_{40:\overline{t|}}\) at \(t = 10.5\).

hints:

Differential reduces to be the EPV of the benefit payment at the upper time limit.

t = 10.5

E = t * SULT().E_r(40, t=t)

isclose(6.239, E, question="Q5.3")

----- Q5.3 6.239: 6.23871918627528 [OK] -----

True

SOA Question 5.4 : (A) 213.7

(40) wins the SOA lottery and will receive both:

A deferred life annuity of K per year, payable continuously, starting at age \(40 + \overset{\circ}{e}_{40}\) and

An annuity certain of K per year, payable continuously, for \(\overset{\circ}{e}_{40}\) years

You are given:

\(\mu = 0.02\)

\(\delta = 0.01\)

The actuarial present value of the payments is 10,000

Calculate K.

hints:

compute certain and life annuity factor as the sum of a certain annuity and a deferred life annuity.

solve for amount of annual benefit that equals given EPV

life = ConstantForce(mu=0.02).set_interest(delta=0.01)

u = life.e_x(40, curtate=False)

P = 10000 / life.certain_life_annuity(40, u=u, discrete=False)

isclose(213.7, P, question="Q5.4") # 213.7

----- Q5.4 213.7: 213.74552118275955 [OK] -----

True

SOA Question 5.5 : (A) 1699.6

For an annuity-due that pays 100 at the beginning of each year that (45) is alive, you are given:

Mortality for standard lives follows the Standard Ultimate Life Table

The force of mortality for standard lives age 45 + t is represented as \(\mu_{45+t}^{SULT}\)

The force of mortality for substandard lives age 45 + t, \(\mu_{45+t}^{S}\), is defined as:

\(i = 0.05\)

Calculate the actuarial present value of this annuity for a substandard life age 45.

hints:

adjust mortality rate for the extra risk

compute annuity by backward recursion.

life = SULT() # start with SULT life table

q = ExtraRisk(life=life, extra=0.05, risk="ADD_FORCE")['q']

select = SelectLife(periods=1).set_select(s=0, age_selected=True, q=q)\

.set_select(s=1, age_selected=False, a=life['a'])\

.set_interest(i=0.05)\

.fill_table()

a = 100 * select['a'][45][0]

isclose(1700, a, question="Q5.5")

----- Q5.5 1700: 1699.60765931901 [OK] -----

True

SOA Question 5.6 : (D) 1200

For a group of 100 lives age x with independent future lifetimes, you are given:

Each life is to be paid 1 at the beginning of each year, if alive

\(A_x = 0.45\)

\(^2A_x = 0.22\)

\(i = 0.05\)

\(Y\) is the present value random variable of the aggregate payments.

Using the normal approximation to \(Y\), calculate the initial size of the fund needed to be 95% certain of being able to make the payments for these life annuities.

hints:

compute mean and variance of EPV of whole life annuity from whole life insurance twin and variance identities.

portfolio percentile of the sum of \(N=100\) life annuity payments

life = Annuity().set_interest(i=0.05)

var = life.annuity_variance(A2=0.22, A1=0.45)

mean = life.annuity_twin(A=0.45)

fund = life.portfolio_percentile(mean, var, prob=.95, N=100)

isclose(1200, fund, question="Q5.6")

----- Q5.6 1200: 1200.6946732201702 [OK] -----

True

SOA Question 5.7 : (C)

You are given:

\(A_{35} = 0.188\)

\(A_{65} = 0.498\)

\(_{30}p_{35} = 0.883\)

\(i = 0.04\)

Calculate \(1000 \ddot{a}^{(2)}_{35:\overline{30|}}\) using the two-term Woolhouse approximation.

hints:

compute endowment insurance from relationships of whole life, temporary and deferred insurances.

compute temporary annuity from insurance twin

apply Woolhouse approximation

life = Recursion().set_interest(i=0.04)\

.set_A(0.188, x=35)\

.set_A(0.498, x=65)\

.set_p(0.883, x=35, t=30)

mthly = Woolhouse(m=2, life=life, three_term=False)

a = 1000 * mthly.temporary_annuity(35, t=30)

isclose(17376.7, a, question="Q5.7")

----- Q5.7 17376.7: 17376.71459632958 [OK] -----

True

SOA Question 5.8 : (C) 0.92118

For an annual whole life annuity-due of 1 with a 5-year certain period on (55), you are given:

Mortality follows the Standard Ultimate Life Table

i = 0.05

Calculate the probability that the sum of the undiscounted payments actually made under this annuity will exceed the expected present value, at issue, of the annuity.

hints:

calculate EPV of certain and life annuity.

find survival probability of lifetime s.t. sum of annual payments exceeds EPV

sult = SULT()

a = sult.certain_life_annuity(55, u=5)

p = sult.p_x(55, t=math.floor(a))

isclose(0.92118, p, question="Q5.8")

----- Q5.8 0.92118: 0.9211799771029529 [OK] -----

True

SOA Question 5.9 : (C) 0.015

hints:

express both EPV’s expressed as forward recursions

solve for unknown constant \(k\).

x, p = 0, 0.9 # set arbitrary p_x = 0.9

a = Recursion().set_a(21.854, x=x)\

.set_p(p, x=x)\

.whole_life_annuity(x+1)

life = Recursion(verbose=False).set_a(22.167, x=x)

def fun(k): return a - life.set_p((1 + k) * p, x=x).whole_life_annuity(x + 1)

k = life.solve(fun, target=0, grid=[0.005, 0.025])

isclose(0.015, k, question="Q5.9")

----- Q5.9 0.015: 0.015009110961925138 [OK] -----

True

6 Premium Calculation#

SOA Question 6.1 : (D) 35.36

6.1. You are given the following information about a special fully discrete 2-payment, 2-year term insurance on (80):

(i) Mortality follows the Standard Ultimate Life Table

(ii) i = 0.03

(iii) The death benefit is 1000 plus a return of all premiums paid without interest

(iv) Level premiums are calculated using the equivalence principle

Calculate the net premium for this special insurance.

[A modified version of Question 22 on the Fall 2012 exam]

hints:

solve net premium such that EPV annuity = EPV insurance + IA factor for returns of premiums without interest

P = SULT().set_interest(i=0.03)\

.net_premium(80, t=2, b=1000, return_premium=True)

isclose(35.36, P, question="Q6.1")

----- Q6.1 35.36: 35.359222861900264 [OK] -----

True

SOA Question 6.2 : (E) 3604

6.2. For a fully discrete 10-year term life insurance policy on (x), you are given:

(i) Death benefits are 100,000 plus the return of all gross premiums paid without interest

(ii) Expenses are 50% of the first year’s gross premium, 5% of renewal gross premiums and 200 per policy expenses each year

(iii) Expenses are payble at the beginnig of the year

(iv) \(A^1_{x:\overline{10|}} = 0.17094\)

(v) \((IA)^1_{x:\overline{10|}} = 0.96728\)

(vi) \(\ddot{a}^1_{x:\overline{10|}} = 6.8865\)

Calculate the gross premium using the equivalence principle.

[Question 25 on the Fall 2012 exam]

hints:

EPV return of premiums without interest = Premium \(\times\) IA factor

solve for gross premiums such that EPV premiums = EPV benefits and expenses

life = Premiums()

A, IA, a = 0.17094, 0.96728, 6.8865

P = life.gross_premium(a=a, A=A, IA=IA, benefit=100000,

initial_premium=0.5, renewal_premium=.05,

renewal_policy=200, initial_policy=200)

isclose(3604, P, question="Q6.2")

----- Q6.2 3604: 3604.229940320728 [OK] -----

True

SOA Question 6.3 : (C) 0.390

S, now age 65, purchased a 20-year deferred whole life annuity-due of 1 per year at age 45. You are given:

Equal annual premiums, determined using the equivalence principle, were paid at the beginning of each year during the deferral period

Mortality at ages 65 and older follows the Standard Ultimate Life Table

i = 0.05

Y is the present value random variable at age 65 for S’s annuity benefits

Calculate the probability that Y is less than the actuarial accumulated value of S’s premiums.

hints:

solve lifetime \(t\) such that PV annuity certain = PV whole life annuity at age 65

calculate mortality rate through the year before curtate lifetime

life = SULT()

t = life.Y_to_t(life.whole_life_annuity(65))

q = 1 - life.p_x(65, t=math.floor(t) - 1)

isclose(0.39, q, question="Q6.3")

----- Q6.3 0.39: 0.39039071872030084 [OK] -----

True

SOA Question 6.4 : (E) 1890

For whole life annuities-due of 15 per month on each of 200 lives age 62 with independent future lifetimes, you are given:

i = 0.06

\(A^{12}_{62} = 0.4075\) and \(^2A^{(12)}_{62} = 0.2105\)

\(\pi\) is the single premium to be paid by each of the 200 lives

S is the present value random variable at time 0 of total payments made to the 200 lives

Using the normal approximation, calculate \(\pi\) such at \(Pr(200 \pi > S) = 0.90\)

mthly = Mthly(m=12, life=Annuity().set_interest(i=0.06))

A1, A2 = 0.4075, 0.2105

mean = mthly.annuity_twin(A1) * 15 * 12

var = mthly.annuity_variance(A1=A1, A2=A2, b=15 * 12)

S = Annuity.portfolio_percentile(mean=mean, variance=var, prob=.9, N=200) / 200

isclose(1890, S, question="Q6.4")

----- Q6.4 1890: 1893.912859650868 [OK] -----

True

SOA Question 6.5 : (D) 33

For a fully discrete whole life insurance of 1000 on (30), you are given:

Mortality follows the Standard Ultimate Life Table

i = 0.05

The premium is the net premium

Calculate the first year for which the expected present value at issue of that year’s premium is less than the expected present value at issue of that year’s benefit.

life = SULT()

P = life.net_premium(30, b=1000)

def gain(k):

return life.Y_x(30, t=k) * P - life.Z_x(30, t=k) * 1000

k = min([k for k in range(100) if gain(k) < 0]) + 1 # add 1 because k=0 is first policy year

isclose(33, k, question="Q6.5")

----- Q6.5 33: 33 [OK] -----

True

SOA Question 6.6 : (B) 0.79

For fully discrete whole life insurance policies of 10,000 issued on 600 lives with independent future lifetimes, each age 62, you are given:

Mortality follows the Standard Ultimate Life Table

i = 0.05

Expenses of 5% of the first year gross premium are incurred at issue

Expenses of 5 per policy are incurred at the beginning of each policy year

The gross premium is 103% of the net premium.

\(_0L\) is the aggregate present value of future loss at issue random variable

Calculate \(Pr( _0L < 40,000)\), using the normal approximation.

life = SULT()

P = life.net_premium(62, b=10000)

contract = Contract(premium=1.03*P,

renewal_policy=5,

initial_policy=5,

initial_premium=0.05,

benefit=10000)

L = life.gross_policy_value(62, contract=contract)

var = life.gross_policy_variance(62, contract=contract)

prob = life.portfolio_cdf(mean=L, variance=var, value=40000, N=600)

isclose(.79, prob, question="Q6.6")

----- Q6.6 0.79: 0.7914321142683529 [OK] -----

True

SOA Question 6.7 : (C) 2880

For a special fully discrete 20-year endowment insurance on (40), you are given:

The only death benefit is the return of annual net premiums accumulated with interest at 5% to the end of the year of death

The endowment benefit is 100,000

Mortality follows the Standard Ultimate Life Table

i = 0.05

Calculate the annual net premium.

life = SULT()

a = life.temporary_annuity(40, t=20)

A = life.E_x(40, t=20)

IA = a - life.interest.annuity(t=20) * life.p_x(40, t=20)

G = life.gross_premium(a=a, A=A, IA=IA, benefit=100000)

isclose(2880, G, question="Q6.7")

----- Q6.7 2880: 2880.2463991134578 [OK] -----

True

SOA Question 6.8 : (B) 9.5

For a fully discrete whole life insurance on (60), you are given:

Mortality follows the Standard Ultimate Life Table

i = 0.05

The expected company expenses, payable at the beginning of the year, are:

50 in the first year

10 in years 2 through 10

5 in years 11 through 20

0 after year 20

Calculate the level annual amount that is actuarially equivalent to the expected company expenses.

hints:

calculate EPV of expenses as deferred life annuities

solve for level premium

life = SULT()

initial_cost = (50 + 10 * life.deferred_annuity(60, u=1, t=9)

+ 5 * life.deferred_annuity(60, u=10, t=10))

P = life.net_premium(60, initial_cost=initial_cost)

isclose(9.5, P, question="Q6.8")

----- Q6.8 9.5: 9.526003201821927 [OK] -----

True

SOA Question 6.9 : (D) 647

life = SULT()

a = life.temporary_annuity(50, t=10)

A = life.term_insurance(50, t=20)

initial_cost = 25 * life.deferred_annuity(50, u=10, t=10)

P = life.gross_premium(a=a, A=A, benefit=100000,

initial_premium=0.42, renewal_premium=0.12,

initial_policy=75 + initial_cost, renewal_policy=25)

isclose(647, P, question="Q6.9")

----- Q6.9 647: 646.8608151974504 [OK] -----

True

SOA Question 6.10 : (D) 0.91

For a fully discrete 3-year term insurance of 1000 on (x), you are given:

\(p_x\) = 0.975

i = 0.06

The actuarial present value of the death benefit is 152.85

The annual net premium is 56.05

Calculate \(p_{x+2}\).

x = 0

life = Recursion(depth=5).set_interest(i=0.06)\

.set_p(0.975, x=x)\

.set_a(152.85/56.05, x=x, t=3)\

.set_A(152.85, x=x, t=3, b=1000)

p = life.p_x(x=x+2)

isclose(0.91, p, question="Q6.10")

----- Q6.10 0.91: 0.9097382950525702 [OK] -----

True

SOA Question 6.11 : (C) 0.041

life = Recursion().set_interest(i=0.04)

A = life.set_A(0.39788, 51)\

.set_q(0.0048, 50)\

.whole_life_insurance(50)

P = life.gross_premium(A=A, a=life.annuity_twin(A=A))

A = life.set_q(0.048, 50).whole_life_insurance(50)

loss = A - life.annuity_twin(A) * P

isclose(0.041, loss, question="Q6.11")

----- Q6.11 0.041: 0.04069206883563675 [OK] -----

True

SOA Question 6.12 : (E) 88900

For a fully discrete whole life insurance of 1000 on (x), you are given:

The following expenses are incurred at the beginning of each year:

Year 1 |

Years 2+ |

|

|---|---|---|

Percent of premium |

75% |

10% |

Maintenance expenses |

10 |

2 |

An additional expense of 20 is paid when the death benefit is paid

The gross premium is determined using the equivalence principle

\(i = 0.06\)

\(\ddot{a}_x = 12.0\)

\(^2A_x = 0.14\)

Calculate the variance of the loss at issue random variable.

life = PolicyValues().set_interest(i=0.06)

a = 12

A = life.insurance_twin(a)

contract = Contract(benefit=1000, settlement_policy=20,

initial_policy=10, initial_premium=0.75,

renewal_policy=2, renewal_premium=0.1)

contract.premium = life.gross_premium(A=A, a=a, **contract.premium_terms)

L = life.gross_variance_loss(A1=A, A2=0.14, contract=contract)

isclose(88900, L, question="Q6.12")

----- Q6.12 88900: 88862.59592874818 [OK] -----

True

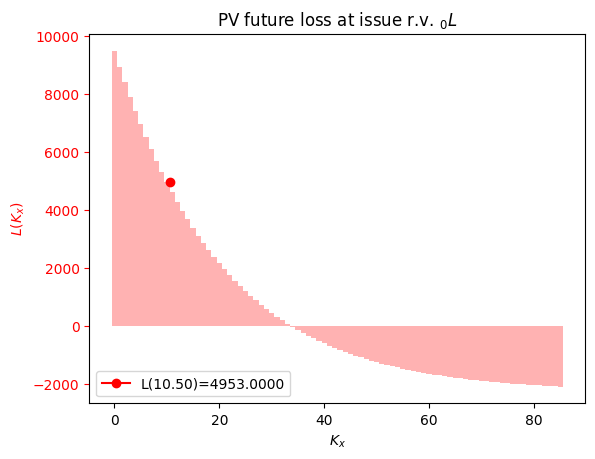

SOA Question 6.13 : (D) -400

For a fully discrete whole life insurance of 10,000 on (45), you are given:

Commissions are 80% of the first year premium and 10% of subsequent premiums. There are no other expenses

Mortality follows the Standard Ultimate Life Table

i = 0.05

\(_0L\) denotes the loss at issue random variable

If \(T_{45} = 10.5\), then \(_0L = 4953\)

Calculate \(E[_0L]\) .

life = SULT().set_interest(i=0.05)

A = life.whole_life_insurance(45)

contract = Contract(benefit=10000, initial_premium=.8, renewal_premium=.1)

def fun(P): # Solve for premium, given Loss(t=0) = 4953

return life.L_from_t(t=10.5, contract=contract.set_contract(premium=P))

contract.set_contract(premium=life.solve(fun, target=4953, grid=100))

L = life.gross_policy_value(45, contract=contract)

life.L_plot(x=45, T=10.5, contract=contract)

isclose(-400, L, question="Q6.13")

----- Q6.13 -400: -400.944475998793 [OK] -----

True

SOA Question 6.14 : (D) 1150

For a special fully discrete whole life insurance of 100,000 on (40), you are given:

The annual net premium is P for years 1 through 10, 0.5P for years 11 through 20, and 0 thereafter

Mortality follows the Standard Ultimate Life Table

i = 0.05

Calculate P.

life = SULT().set_interest(i=0.05)

a = life.temporary_annuity(40, t=10) + 0.5*life.deferred_annuity(40, u=10, t=10)

A = life.whole_life_insurance(40)

P = life.gross_premium(a=a, A=A, benefit=100000)

isclose(1150, P, question="Q6.14")

----- Q6.14 1150: 1148.5800555155258 [OK] -----

True

SOA Question 6.15 : (B) 1.002

For a fully discrete whole life insurance of 1000 on (x) with net premiums payable quarterly, you are given:

\(i = 0.05\)

\(\ddot{a}_x = 3.4611\)

\(P^{(W)}\) and \(P^{(UDD)}\) are the annualized net premiums calculated using the 2-term Woolhouse (W) and the uniform distribution of deaths (UDD) assumptions, respectively

Calculate \(\dfrac{P^{(UDD)}}{P^{(W)}}\).

life = Recursion().set_interest(i=0.05).set_a(3.4611, x=0)

A = life.insurance_twin(3.4611)

udd = UDD(m=4, life=life)

a1 = udd.whole_life_annuity(x=x)

woolhouse = Woolhouse(m=4, life=life)

a2 = woolhouse.whole_life_annuity(x=x)

P = life.gross_premium(a=a1, A=A)/life.gross_premium(a=a2, A=A)

isclose(1.002, P, question="Q6.15")

----- Q6.15 1.002: 1.0022973504113772 [OK] -----

True

SOA Question 6.16 : (A) 2408.6

For a fully discrete 20-year endowment insurance of 100,000 on (30), you are given:

d = 0.05

Expenses, payable at the beginning of each year, are:

First Year |

First Year |

Renewal Years |

Renewal Years |

|

|---|---|---|---|---|

Percent of Premium |

Per Policy |

Percent of Premium |

Per Policy |

|

Taxes |

4% |

0 |

4% |

0 |

Sales Commission |

35% |

0 |

2% |

0 |

Policy Maintenance |

0% |

250 |

0% |

50 |

The net premium is 2143

Calculate the gross premium using the equivalence principle.

life = Premiums().set_interest(d=0.05)

A = life.insurance_equivalence(premium=2143, b=100000)

a = life.annuity_equivalence(premium=2143, b=100000)

p = life.gross_premium(A=A, a=a, benefit=100000, settlement_policy=0,

initial_policy=250, initial_premium=0.04 + 0.35,

renewal_policy=50, renewal_premium=0.04 + 0.02)

isclose(2410, p, question="Q6.16")

----- Q6.16 2410: 2408.575206281868 [OK] -----

True

SOA Question 6.17 : (A) -30000

An insurance company sells special fully discrete two-year endowment insurance policies to smokers (S) and non-smokers (NS) age x. You are given:

The death benefit is 100,000; the maturity benefit is 30,000

The level annual premium for non-smoker policies is determined by the equivalence principle

The annual premium for smoker policies is twice the non-smoker annual premium

\(\mu^{NS}_{x+t} = 0.1.\quad t > 0\)

\(q^S_{x+k} = 1.5 q_{x+k}^{NS}\), for \(k = 0, 1\)

\(i = 0.08\)

Calculate the expected present value of the loss at issue random variable on a smoker policy.

x = 0

life = ConstantForce(mu=0.1).set_interest(i=0.08)

A = life.endowment_insurance(x, t=2, b=100000, endowment=30000)

a = life.temporary_annuity(x, t=2)

P = life.gross_premium(a=a, A=A)

life1 = Recursion().set_interest(i=0.08)\

.set_q(life.q_x(x, t=1) * 1.5, x=x, t=1)\

.set_q(life.q_x(x+1, t=1) * 1.5, x=x+1, t=1)

contract = Contract(premium=P*2, benefit=100000, endowment=30000)

L = life1.gross_policy_value(x, t=0, n=2, contract=contract)

isclose(-30000, L, question="Q6.17")

----- Q6.17 -30000: -30107.42633581128 [OK] -----

True

SOA Question 6.18 : (D) 166400

For a 20-year deferred whole life annuity-due with annual payments of 30,000 on (40), you are given:

The single net premium is refunded without interest at the end of the year of death if death occurs during the deferral period

Mortality follows the Standard Ultimate Life Table

i = 0.05

Calculate the single net premium for this annuity.

life = SULT().set_interest(i=0.05)

def fun(P):

A = (life.term_insurance(40, t=20, b=P)

+ life.deferred_annuity(40, u=20, b=30000))

return life.gross_premium(a=1, A=A) - P

P = life.solve(fun, target=0, grid=[162000, 168800])

isclose(166400, P, question="Q6.18")

----- Q6.18 166400: 166362.83871487685 [OK] -----

True

SOA Question 6.19 : (B) 0.033

life = SULT()

contract = Contract(initial_policy=.2, renewal_policy=.01)

a = life.whole_life_annuity(50)

A = life.whole_life_insurance(50)

contract.premium = life.gross_premium(A=A, a=a, **contract.premium_terms)

L = life.gross_policy_variance(50, contract=contract)

isclose(0.033, L, question="Q6.19")

----- Q6.19 0.033: 0.03283273381910881 [OK] -----

True

SOA Question 6.20 : (B) 459

For a special fully discrete 3-year term insurance on (75), you are given:

The death benefit during the first two years is the sum of the net premiums paid without interest

The death benefit in the third year is 10,000

\(x\) |

\(p_x\) |

|---|---|

75 |

0.90 |

76 |

0.88 |

77 |

0.85 |

\(i = 0.04\)

Calculate the annual net premium.

life = LifeTable().set_interest(i=.04).set_table(p={75: .9, 76: .88, 77: .85})

a = life.temporary_annuity(75, t=3)

IA = life.increasing_insurance(75, t=2)

A = life.deferred_insurance(75, u=2, t=1)

def fun(P): return life.gross_premium(a=a, A=P*IA + A*10000) - P

P = life.solve(fun, target=0, grid=[449, 489])

isclose(459, P, question="Q6.20")

----- Q6.20 459: 458.83181728297365 [OK] -----

True

SOA Question 6.21 : (C) 100

life = Recursion(verbose=False).set_interest(d=0.04)

life.set_A(0.7, x=75, t=15, endowment=1)

life.set_E(0.11, x=75, t=15)

def fun(P):

return (P * life.temporary_annuity(75, t=15) -

life.endowment_insurance(75, t=15, b=1000, endowment=15*float(P)))

P = life.solve(fun, target=0, grid=(80, 120))

isclose(100, P, question="Q6.21")

----- Q6.21 100: 100.85470085470084 [OK] -----

/tmp/ipykernel_20933/899435277.py:6: DeprecationWarning: Conversion of an array with ndim > 0 to a scalar is deprecated, and will error in future. Ensure you extract a single element from your array before performing this operation. (Deprecated NumPy 1.25.)

life.endowment_insurance(75, t=15, b=1000, endowment=15*float(P)))

True

SOA Question 6.22 : (C) 102

For a whole life insurance of 100,000 on (45) with premiums payable monthly for a period of 20 years, you are given:

The death benefit is paid immediately upon death

Mortality follows the Standard Ultimate Life Table

Deaths are uniformly distributed over each year of age

\(i = 0.05\)

Calculate the monthly net premium.

life=SULT(udd=True)

a = UDD(m=12, life=life).temporary_annuity(45, t=20)

A = UDD(m=0, life=life).whole_life_insurance(45)

P = life.gross_premium(A=A, a=a, benefit=100000) / 12

isclose(102, P, question="Q6.22")

----- Q6.22 102: 102.40668704849178 [OK] -----

True

SOA Question 6.23 : (D) 44.7

x = 0

life = Recursion().set_a(15.3926, x=x)\

.set_a(10.1329, x=x, t=15)\

.set_a(14.0145, x=x, t=30)

def fun(P):

per_policy = 30 + (30 * life.whole_life_annuity(x))

per_premium = (0.6 + 0.1*life.temporary_annuity(x, t=15)

+ 0.1*life.temporary_annuity(x, t=30))

a = life.temporary_annuity(x, t=30)

return (P * a) - (per_policy + per_premium * P)

P = life.solve(fun, target=0, grid=[30.3, 49.5])

isclose(44.7, P, question="Q6.23")

----- Q6.23 44.7: 44.70806635781145 [OK] -----

True

SOA Question 6.24 : (E) 0.30

For a fully continuous whole life insurance of 1 on (x), you are given:

L is the present value of the loss at issue random variable if the premium rate is determined by the equivalence principle

L^* is the present value of the loss at issue random variable if the premium rate is 0.06

\(\delta = 0.07\)

\(\overline{A}_x = 0.30\)

\(Var(L) = 0.18\)

Calculate \(Var(L^*)\).

life = PolicyValues().set_interest(delta=0.07)

x, A1 = 0, 0.30 # Policy for first insurance

P = life.premium_equivalence(A=A1, discrete=False) # Need its premium

contract = Contract(premium=P, discrete=False)

def fun(A2): # Solve for A2, given Var(Loss)

return life.gross_variance_loss(A1=A1, A2=A2, contract=contract)

A2 = life.solve(fun, target=0.18, grid=0.18)

contract = Contract(premium=0.06, discrete=False) # Solve second insurance

var = life.gross_variance_loss(A1=A1, A2=A2, contract=contract)

isclose(0.304, var, question="Q6.24")

----- Q6.24 0.304: 0.30419999999999975 [OK] -----

True

SOA Question 6.25 : (C) 12330

For a fully discrete 10-year deferred whole life annuity-due of 1000 per month on (55), you are given:

The premium, \(G\), will be paid annually at the beginning of each year during the deferral period

Expenses are expected to be 300 per year for all years, payable at the beginning of the year

Mortality follows the Standard Ultimate Life Table

\(i = 0.05\)

Using the two-term Woolhouse approximation, the expected loss at issue is -800

Calculate \(G\).

life = SULT()

woolhouse = Woolhouse(m=12, life=life)

benefits = woolhouse.deferred_annuity(55, u=10, b=1000 * 12)

expenses = life.whole_life_annuity(55, b=300)

payments = life.temporary_annuity(55, t=10)

def fun(P):

return life.gross_future_loss(A=benefits + expenses, a=payments,

contract=Contract(premium=P))

P = life.solve(fun, target=-800, grid=[12110, 12550])

isclose(12330, P, question="Q6.25")

----- Q6.25 12330: 12325.781125438532 [OK] -----

True

SOA Question 6.26 : (D) 180

For a special fully discrete whole life insurance policy of 1000 on (90), you are given:

The first year premium is 0

P is the renewal premium

Mortality follows the Standard Ultimate Life Table

i = 0.05

Premiums are calculated using the equivalence principle

Calculate P.

life = SULT().set_interest(i=0.05)

def fun(P):

return P - life.net_premium(90, b=1000, initial_cost=P)

P = life.solve(fun, target=0, grid=[150, 190])

isclose(180, P, question="Q6.26")

----- Q6.26 180: 180.03164891315893 [OK] -----

True

SOA Question 6.27 : (D) 10310

For a special fully continuous whole life insurance on (x), you are given:

Premiums and benefits:

First 20 years |

After 20 years |

|

|---|---|---|

Premium Rate |

3P |

P |

Benefit |

1,000,000 |

500,000 |

\(\mu_{x+t} = 0.03, \quad t \ge 0\)

\(\delta = 0.06\)

Calculate \(P\) using the equivalence principle.

life = ConstantForce(mu=0.03).set_interest(delta=0.06)

x = 0

payments = (3 * life.temporary_annuity(x, t=20, discrete=False)

+ life.deferred_annuity(x, u=20, discrete=False))

benefits = (1000000 * life.term_insurance(x, t=20, discrete=False)

+ 500000 * life.deferred_insurance(x, u=20, discrete=False))

P = benefits / payments

isclose(10310, P, question="Q6.27")

----- Q6.27 10310: 10309.617799001708 [OK] -----

True

SOA Question 6.28 : (B) 36

life = SULT().set_interest(i=0.05)

a = life.temporary_annuity(40, t=5)

A = life.whole_life_insurance(40)

P = life.gross_premium(a=a, A=A, benefit=1000,

initial_policy=10, renewal_premium=.05,

renewal_policy=5, initial_premium=.2)

isclose(36, P, question="Q6.28")

----- Q6.28 36: 35.72634219391481 [OK] -----

True

SOA Question 6.29 : (B) 20.5

(35) purchases a fully discrete whole life insurance policy of 100,000. You are given:

The annual gross premium, calculated using the equivalence principle, is 1770

The expenses in policy year 1 are 50% of premium and 200 per policy

The expenses in policy years 2 and later are 10% of premium and 50 per policy

All expenses are incurred at the beginning of the policy year

\(i = 0.035\)

Calculate \(\ddot{a}_{35}\).

life = Premiums().set_interest(i=0.035)

def fun(a):

return life.gross_premium(A=life.insurance_twin(a=a), a=a,

initial_policy=200, initial_premium=.5,

renewal_policy=50, renewal_premium=.1,

benefit=100000)

a = life.solve(fun, target=1770, grid=[20, 22])

isclose(20.5, a, question="Q6.29")

----- Q6.29 20.5: 20.480268314431726 [OK] -----

True

SOA Question 6.30 : (A) 900

For a fully discrete whole life insurance of 100 on (x), you are given:

The first year expense is 10% of the gross annual premium

Expenses in subsequent years are 5% of the gross annual premium

The gross premium calculated using the equivalence principle is 2.338

\(i = 0.04\)

\(\ddot{a}_x = 16.50\)

\(^2A_x = 0.17\)

Calculate the variance of the loss at issue random variable.

life = PolicyValues().set_interest(i=0.04)

contract = Contract(premium=2.338,

benefit=100,

initial_premium=.1,

renewal_premium=0.05)

var = life.gross_variance_loss(A1=life.insurance_twin(16.50),

A2=0.17, contract=contract)

isclose(900, var, question="Q6.30")

----- Q6.30 900: 908.141412994607 [OK] -----

True

SOA Question 6.31 : (D) 1330

For a fully continuous whole life insurance policy of 100,000 on (35), you are given: